نقابة وسطاء التأمين في لبنان تحت المجهر، هذه الأيام، وقد تكون أوّل مكوّنات قطاع التأمين الذي تُفتح أبواب الإصلاح أمامه، في إطار ورشة كبرى بدأها وزير الإقتصاد والتجارة د. عامر البساط قبل فترة. ومعروف عن قطاع التأمين ككلّ، بقاؤه صلباً ومتماسكاً في وجه الأوضاع المأساوية التي عاشها ولا يزال، في وقت لم يستطع القطاع المصرفي المتقدّم على التأمين بسبب قوته ومكانته وملاءته، من الصمود، اذ تعرّض لأسوأ محنة لم تستطع الحكومة، حتى الآن، من انتشاله من فجوة وقع فيها.

ولأن وسطاء التأمين هم المدماك الأساس للقطاع كونهم يساهمون في تجميع الأقساط والأرباح وتقديم الخدمات لشركات التأمين بنسبة تصل الى 45 بالمئة من المجموع العام… وبما أن الوسطاء أيضاً يقومون بالمهمة الأصعب: وهي تقديم الشروح لكل طالب تغطية وتوضيح البنود التي تتضمنها البوالص، فإن وزير الإقتصاد د. عامر البساط قرّر، على ما يبدو، أن يبدأ عملية الإصلاح من هذا المكوّن الأساس، وبلا شكّ كان محقاً.

ويرتكز هذا الإصلاح الذي طرحه البساط على ثلاثة أعمدة: الملاءة الوازنة للشركة حتى تفي بإلتزاماتها، ومن أجل ذلك ألزم الوسيط برفع الكفالة الى خمسين ألف دولار مقسّطة على ثلاث سنوات وفق جدول زمني، على أن يكون القسط الأول عشرين ألف دولار. الثاني، زيادة متطلبات رأس المال، إعتماد مدوّنة سلوك مهنيّة، توضيح آليات العمولات ووضع ضمانات صارمة لحماية أموال المؤّمن لهم. ثالثاً، إخضاع هذا المكوّن التأميني لرقابة مشدّدة، بحيث يتمّ تحديد نشاط الوسطاء غير المرخصين وحوكمة القطاع عبر إعادة تفعيل “المجلس الوطني للضمان”.

هذا المقترح الذي ناقشه وزير الإقتصاد مع مجلس نقابة الوسطاء بوصف وزارته قيّمة على قطاع التأمين ككلّ، لم يلقَ ترحيباً بالمُطلق، كما لم يلقَ اعتراضاً بالمطلق أيضاً، وهذا طبيعي ولأسباب عديدة لن ندخل في تفاصيلها، مع العلم أن المقترح، بحد ذاته، كان عرضة لأخذ ورد وجدل لا يزال دائراً حتى الساعة.

نقيب الوسطاء الأسبق سليم يارد، الرئيس التنفيذي والمدير العام لشركة Sloop للوساطة التأمينية والإستشارات والباحث في الشأن التأميني وله دراسات ومقالات في هذا المجال، والمحاضر في معهد العلوم التأمينية التابع لجامعة القديس يوسف ISSA ، الى جانب كونه عضواً في الهيئة الإستشارية لهذا المعهد وعضواً في مجلس التوجيه الإستراتيجي له، قرّر حسم الجدل بدراسة علمية أعدها قبل أيام، ركّز فيها على تجارب دول أخرى في موضوع تطوير مهنة وساطة التأمين مع اقتراح أفكار لحلول قابلة للتنفيذ وإستيعاب المعترضين، وكل ذلك للنهوض بهذا القطاع الذي يبقى المدماك الأساس، كما أسلفنا، لقطاع التأمين اللبناني ككل.

الدراسة كتبها سليم يارد باللغة الإنكليزية. وتعميماً للفائدة قرّر أيضاً نشرها باللغتين العربية والفرنسية لتكون في متناول الجميع. ويكفي للقارئ أن يضغط على أحد الرابطَيْن المرفقَيْن ليختار اللغة التي يودّ الإطلاع عبرها على هذه الدراسة القيمّة، معتمداً على علمه وثقافته وقراءاته ومتبعاته ومحبته لهذه المهنة التي طوّرها بأساليب ذكية خاصة به، من بينها ان الوثيقة التي يتسلّمها العميل محرّرة على قياسه ووفق رغباته…

في ما يلي النص باللغة الإنجليزية، ومن يودّ الاطلاع على الدراسة باللغة العربية أو الفرنسية، يمكنه الضغط على الرابطين المرفقين:

Salim-Yared-Ar.pdf Salim Yared Fr

FINANCIAL SOUNDNESS

IN INSURANCE BROKERAGE

Comparative Regulatory Approach

and Review of Lebanon’s $50,000.00 Letter of Guarantee

*Prepared by Salim Yared

Insurance Brokers and Financial Soundness

Insurance brokers play a vital role in connecting policyholders with insurance companies. Unlike insurers, brokers do not assume risk. Instead, they advise clients, identify appropriate coverage, negotiate with insurers, and assist policyholders throughout the insurance lifecycle. Because brokers provide professional advice and, in some jurisdictions, may handle client funds, they occupy a position of trust that requires competence, integrity, and financial responsibility.

For this reason, insurance brokerage is a regulated profession in most jurisdictions. Licensing requirements are designed to protect consumers, promote confidence in the insurance market, and ensure that brokers are capable of fulfilling their professional obligations. While regulatory models differ, they generally assess brokers using a combination of professional qualifications, ethical standards, financial soundness, and ongoing regulatory oversight rather than any single requirement.

Financial soundness is one component of this broader framework. It should not be confused with professional competence or consumer protection measures such as professional indemnity insurance. Instead, it demonstrates that a broker has the financial capacity to operate responsibly and maintain confidence in the marketplace. Different jurisdictions achieve this objective through minimum capital requirements, bank guarantees, professional indemnity insurance, client-money safeguards, or combinations of these tools.

The purpose of this paper is to examine how internationally recognized regulatory frameworks assess the financial soundness of insurance brokers and to compare those approaches with the Lebanese requirement for a $50,000.00 letter of guarantee. Rather than advocating for or against any single regulatory mechanism, this paper evaluates whether Lebanon’s approach is consistent with international principles and identifies opportunities to strengthen the overall regulatory framework.

The Evolution of Insurance Broker Regulation

Insurance broker regulation has evolved significantly over the past several decades. Historically, licensing focused on basic eligibility requirements such as age, experience, and good character. As insurance products became more sophisticated and consumer protection emerged as a greater regulatory priority, supervisory authorities adopted a more comprehensive approach.

Today, most mature regulatory systems evaluate brokers using a “Fit and Proper” framework. Although terminology varies by jurisdiction, the concept generally includes five core elements:

– Professional competence

– Integrity and good reputation

– Financial soundness

– Appropriate governance and internal controls

– Compliance with applicable laws and regulations

his holistic approach recognizes that no single requirement is sufficient to demonstrate a broker’s suitability. A financially strong broker who lacks competence or integrity presents risks to consumers, just as a technically qualified broker without adequate financial resources may struggle to operate responsibly.

International standards therefore focus on regulatory outcomes rather than prescribing one uniform licensing model. Some jurisdictions rely on minimum capital requirements, others require professional indemnity insurance or client-money protections, while some incorporate bank guarantees as evidence of financial responsibility. Although the regulatory tools differ, the objective remains the same: ensuring that insurance brokers are financially reliable, professionally competent, and capable of protecting policyholders.

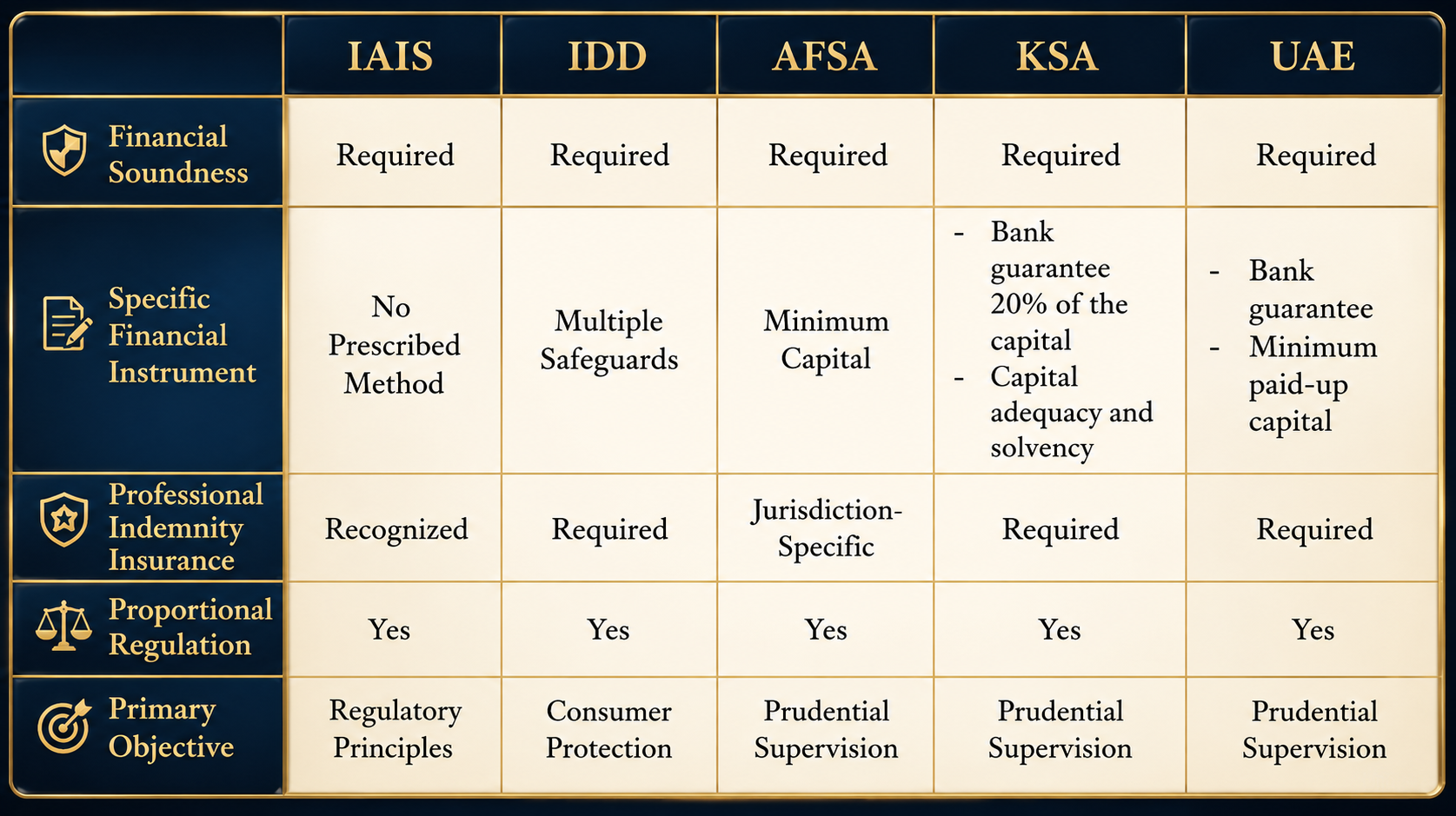

This framework provides the basis for the chapters that follow, which compare the approaches adopted by the IAIS, the European Union’s Insurance Distribution Directive (IDD), the Astana Financial Services Authority (AFSA), Saudi Arabia(SAMA), the Central Bank of the United Arab Emirates (CBUAE). and Lebanon.

International Regulatory Approaches to Financial Soundness

Internationally, insurance regulators share a common objective: ensuring that insurance brokers are professionally competent, financially reliable, and capable of protecting policyholders. While the mechanisms used to achieve this objective vary across jurisdictions, there is broad agreement that financial soundness is an essential component of broker regulation.

The following comparison examines five influential regulatory models: the International Association of Insurance Supervisors, the European Union’s Insurance Distribution Directive, the Astana Financial Services Authority, Saudi Arabia(SAMA) and the United Arab Emirates (UAE).

Association of Insurance Supervisors (IAIS) Framework

The IAIS establishes internationally recognized supervisory principles rather than prescriptive rules.

Its Insurance Core Principles emphasize professionalism, integrity, competence, consumer protection, and financial soundness, while allowing each jurisdiction flexibility in determining how those objectives are achieved.

Importantly, the IAIS does not mandate a specific bank guarantee, capital requirement, or professional indemnity insurance threshold. Instead, it expects regulators to ensure that intermediaries maintain financial resources appropriate to the nature and scale of their activities.

European Union’s Insurance Distribution Directive (IDD)

The European Union adopts a comprehensive, risk-based approach to regulation. Rather than relying on a single financial instrument, the IDD combines professional competence, continuing education, good repute, professional indemnity insurance, client-money protection, governance requirements, and ongoing supervision. Although the IDD does not require a fixed bank guarantee, it incorporates multiple safeguards that collectively demonstrate financial soundness and protect consumers.

Astana Financial Services Authority (AFSA) Model

The AFSA focuses on prudential regulation through minimum capital requirements. Instead of requiring a letter of guarantee, AFSA requires intermediaries to maintain capital resources that reflect the size and risk profile of their business. This proportional approach recognizes that larger firms and firms handling client money present greater operational risks and therefore require stronger financial resources.

Saudi Arabia – Saudi Central Bank (SAMA)

The Kingdom of Saudi Arabia adopts one of the most stringent prudential regulatory frameworks for insurance intermediaries in the region. The Saudi Central Bank (SAMA) requires insurance brokers to demonstrate substantial financial capacity before being granted a license.

The Saudi regulatory model demonstrates that financial soundness is assessed through multiple complementary safeguards rather than a single licensing requirement. Paid-up capital, banking support, professional indemnity insurance and ongoing prudential supervision collectively ensure that licensed brokers remain financially stable throughout their operations.

United Arab Emirates (UAE)-Central Bank of the United Arab Emirates (CBUAE)

The United Arab Emirates similarly applies a comprehensive prudential framework for insurance brokers through its insurance regulatory regime.

Rather than relying exclusively on a bank guarantee, the UAE combines minimum capital requirements, bank guarantees, professional indemnity insurance, corporate governance, and ongoing financial supervision.

The CBUAE regulatory framework recognizes that financial soundness extends beyond initial licensing and requires continuous compliance with prudential standards throughout the broker’s operations.

→Comparative Analysis Findings

Despite using different regulatory tools, all five frameworks reach the same conclusion: financial soundness is a fundamental licensing requirement. The principal difference lies in how that requirement is demonstrated.

The IAIS establishes broad supervisory principles; the European Union relies on a combination of regulatory safeguards; AFSA emphasizes minimum capital requirements; Saudi Arabia (SAMA) requires insurance brokers to demonstrate substantial financial capacity before being granted a license, and the Central Bank of the United Arab Emirates (CBUAE) requires continuous compliance with prudential standards throughout the broker’s operations.

None of these frameworks requires a single universal model, reinforcing the principle that jurisdictions may adopt different mechanisms while pursuing the same regulatory objective.

This comparative analysis provides the framework for evaluating Lebanon’s $50,000.00 letter of guarantee. The relevant question is not whether Lebanon uses the same mechanism as other jurisdictions, but whether its requirement contributes to the internationally recognized objective of ensuring financially sound and professionally responsible insurance brokers.

The Lebanese Regulatory Framework

Recent Requirement of the $50,000.00 Letter of Guarantee

Lebanon has long required insurance brokers to demonstrate more than technical competence before obtaining a license. The regulatory framework combines education, practical experience, good reputation, and financial responsibility to ensure that licensed brokers are capable of properly serving policyholders and maintaining confidence in the insurance market.

The recent requirement for a $50,000.00 letter of guarantee should therefore be viewed as part of an existing licensing framework rather than an entirely new regulatory concept.

Evolution of the Guarantee

The requirement for a financial guarantee has existed in Lebanese insurance regulation for many years. Its original purpose was to demonstrate a broker’s financial commitment as a condition of licensing. Following Lebanon’s financial crisis and the depreciation of the Lebanese pound, the practical value of the existing guarantee was significantly reduced. The increase to $50,000.00 was intended to restore the economic effectiveness of a longstanding requirement rather than introduce a new regulatory obligation.

Purpose of the Letter of Guarantee

A central theme in the current debate is the purpose of the letter of guarantee. International experience shows that different financial safeguards serve different regulatory objectives. A letter of guarantee is not designed to replace professional indemnity insurance, compensate clients for professional negligence, or secure all premiums collected by brokers. Instead, it demonstrates financial responsibility and provides regulators with evidence that a broker has the financial capacity and banking support necessary to operate within a regulated profession.

International Context

The comparative review of the IAIS, the European Union, the AFSA, SAMA, and the CBUAE demonstrates that financial soundness is a universal regulatory objective, but there is no single internationally accepted method for demonstrating it.

Some jurisdictions rely on minimum capital requirements, others emphasize professional indemnity insurance and client-money safeguards, while Lebanon continues to use a letter of guarantee. These approaches differ in design but pursue the same objective: promoting confidence in insurance intermediaries and protecting policyholders.

Key Considerations→

The debate surrounding the $50,000.00 letter of guarantee should therefore be viewed within the broader context of international insurance regulation.

The key question is not whether Lebanon should mirror another jurisdiction’s regulatory model, but whether its framework effectively demonstrates financial soundness while protecting policyholders and maintaining confidence in the insurance market.

As international practice shows, the letter of guarantee can remain a legitimate component of Lebanon’s licensing framework when supported by additional regulatory safeguards and ongoing supervision.

Financial Soundness:

Remains an internationally recognized licensing requirement.

Letter of Guarantee:

Demonstrates financial responsibility but is not a substitute for other safeguards.

International Practice:

Different jurisdictions use different regulatory tools.

Future Reform:

Additional measures such as professional indemnity insurance, client-money protections, and enhanced supervision could complement the existing framework.

Key Questions Raised by Insurance Brokers

The introduction of the $50,000.00 letter of guarantee has prompted important questions from the insurance brokerage community. These questions are valid and should be considered in light of international regulatory practice. The following section summarizes the principal concerns and how they compare with international standards.

Is $50,000.00 Enough to Protect Clients?

International Perspective:

International frameworks do not rely on a fixed guarantee to compensate clients for professional negligence. That role is typically fulfilled by Professional Indemnity Insurance.

Key Takeaway:

A letter of guarantee is not intended to replace Professional Indemnity Insurance.

Can the Guarantee Secure all Premiums Collected by Brokers?

International Perspective:

Client money is generally protected through segregated accounts, fiduciary controls, reconciliation procedures, or prudential supervision rather than a fixed financial guarantee.

Key Takeaway:

Additional client-money safeguards are needed regardless of the guarantee.

Why Does Europe not Require a Letter of Guarantee?

International Perspective: The European Union uses multiple safeguards, including Professional Indemnity Insurance, governance requirements, client-money protection, continuing education, and regulatory supervision

Key Takeaway:

Europe uses a different regulatory model—not fewer regulatory safeguards.

Does the Guarantee Have a Legitimate Regulatory Purpose?

International Perspective: Many jurisdictions require brokers to demonstrate financial soundness through different mechanisms, including minimum capital, guarantees, or other prudential measures.

Key Takeaway:

The guarantee serves as evidence of financial responsibility rather than comprehensive consumer protection.

Does the Requirement Disproportionately Affect Smaller Brokers?

International Perspective: International regulators increasingly apply proportionality, tailoring requirements to the size and risk profile of regulated firms.

Key Takeaway: Lebanon may wish to consider proportional reforms while preserving the principle of financial soundness.

→ Overall Assessment

The international comparison demonstrates that the debate should not focus solely on whether a letter of guarantee exists. Rather, the relevant question is whether Lebanon’s regulatory framework effectively demonstrates financial soundness while protecting policyholders and supporting confidence in the insurance market. International practice confirms that financial soundness is a universal objective, although the mechanisms used to achieve it vary across jurisdictions.

Instead of viewing the guarantee as the only regulatory safeguard, Lebanon could strengthen its framework by complementing the existing requirement with additional measures such as Professional Indemnity Insurance, enhanced client-money protections, proportional supervision, and stronger governance standards. Such an approach would align more closely with international best practices while maintaining the underlying objective of financial responsibility.

Recommendations for Strengthening Lebanon’s Insurance Brokerage Framework

The comparative analysis demonstrates that financial soundness is a consistent feature of modern insurance regulation, even though jurisdictions use different regulatory tools to achieve it. Rather than focusing solely on the $50,000.00 letter of guarantee, Lebanon has an opportunity to strengthen its overall supervisory framework by adopting complementary measures that reflect international best practices.

– Maintain Financial Soundness Requirements

Retain a requirement demonstrating financial responsibility while periodically reviewing whether the current mechanism remains appropriate for the Lebanese market.

– Introduce Professional Indemnity Insurance

Consider requiring professional indemnity insurance to protect policyholders against losses arising from professional negligence. This complements, rather than replaces, the letter of guarantee.

– Strengthen Client-Money Protection

Where brokers handle premiums or claim payments, adopt safeguards such as segregated client accounts, reconciliation procedures, and periodic reporting.

– Expand Continuing Professional Development

Require ongoing professional education to ensure brokers maintain current knowledge of insurance law, regulation, ethics, and emerging risks.

– Promote Strong Governance

Encourage brokerage firms to adopt internal controls, compliance policies, conflict-of-interest procedures, cybersecurity measures, and business continuity planning.

– Apply Proportional Regulation

Consider risk-based requirements that reflect the size and complexity of brokerage firms while maintaining consistent regulatory objectives.

– Enhance Regulatory Dialogue

Establish a structured consultation process between the Lebanese Insurance Brokers Syndicate (LIBS) and the Insurance Control Commission (ICC) to discuss future reforms and implementation challenges.

Implementation Roadmap→

International practice confirms that there is no single model for regulating insurance brokers. What unites mature regulatory systems is a commitment to professional competence, integrity, financial soundness, consumer protection, and effective supervision.

Lebanon’s letter of guarantee can continue to serve as one element of that framework, provided it is supported by complementary regulatory safeguards. A balanced approach will help strengthen confidence in the insurance market while supporting the long-term professionalism of the brokerage sector.

Short Term––Priority Actions:

International regulators continue to increasingly apply proportionality, tailoring the requirements to the size and risk profile of regulated firms.

Medium Term––Priority Actions:

Introduction of a Professional Indemnity Insurance; strengthening client-money safeguards; and adopting governance standards.

Long Term––Priority Actions:

Implementation of proportional supervision; enhancement of reporting; and development of comprehensive “Fit and Proper” framework.

Former President*

Lebanese Insurance Brokers Syndicate (LIBS)

Chairman & General Manager

Sloop Insurance Brokerage Firm SAL

Insurance & Risk Management Consultant

Lecturer in Insurance

Member of the Academic Committee

Institut Supérieur des Sciences de l’Assurance (ISSA)

Université Saint-Joseph de Beyrouth (USJ)

Member of the Strategic Orientation Council

Institut Supérieur des Sciences de l’Assurance (ISSA)

Université Saint-Joseph de Beyrouth (USJ)

Member of the Institute Board

Institut Supérieur des Sciences de l’Assurance (ISSA)

Université Saint-Joseph de Beyrouth (USJ)